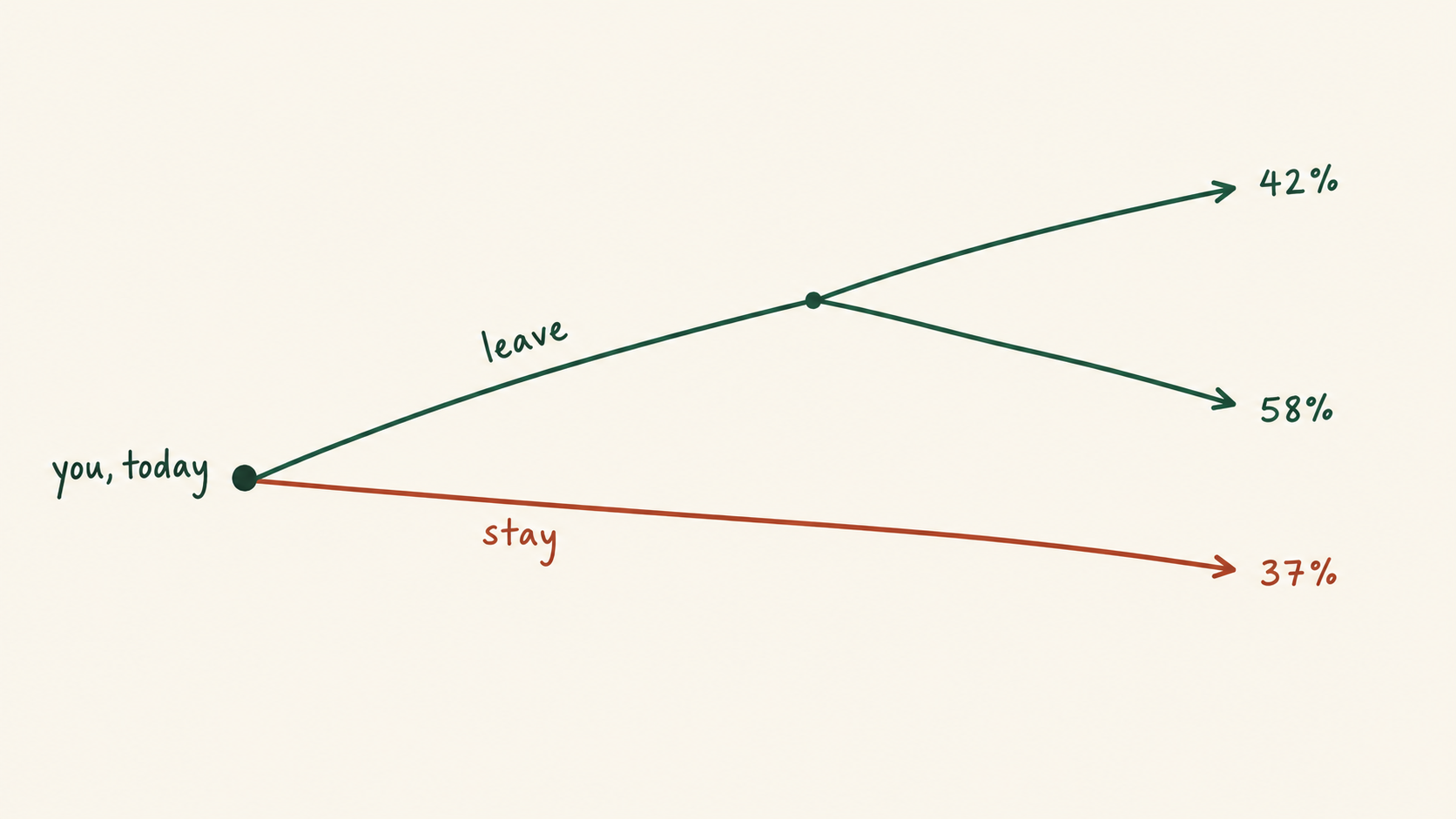

The safe choice feels like the absence of a choice. You stay in the job, the city, the field — and because nothing visibly changes, it registers as zero risk. But there is no no-decision. Staying put is a branch off the same root as everything else, and it carries its own downside: skills that stagnate while the field moves on, an industry that quietly declines underneath you, a wellbeing curve that flattens into a low plateau you stop noticing because you're standing on it. The baseline has an expected value too. Refusing to compute it doesn't make it zero — it just means you're betting blind.

The default that doesn't feel like a bet

The trick the safe choice plays on you is that it doesn't announce itself. When you take the new job or move across the country, you feel the decision — the weighing, the sweaty palms, the irreversibility. When you stay, nothing announces a thing. Tomorrow looks like today, and today looked fine, so the mind files it under "no action taken."

But you did take an action. You re-upped. Every morning you don't change course, you are placing the same chips on the same square, and a year of mornings is a substantial bet. The reason it doesn't feel like one is that the alternatives are invisible. The job you didn't take, the city you didn't move to, the skill you didn't spend the year building — those don't show up as losses on any statement, so they don't show up at all. The price tag of staying is the whole set of branches you declined to walk, and that price is real whether or not you ever read it.

Opportunity cost is the most expensive thing nobody puts on the bill.

Three ways the baseline goes bad

When the safe choice does fail, it rarely fails like a movie. There's no cliff, no single catastrophic morning. It's a slow leak, and that's exactly why it's so easy to miss. It comes in three flavors.

The first is skill stagnation. The field keeps moving and you don't. The work you do this year is the work you did last year, so the gap between what you can do and what the market now wants widens a notch at a time — invisibly, until the day you need to compete and find the ground has shifted under you.

The second is sector decline. Your skills can stay sharp while the thing they're sharp for quietly loses value. Industries contract over a decade, not a day; the people inside them are usually the last to feel it, because from the inside every year looks roughly like the last one. The tide goes out slowly enough that you don't notice you're aground.

The third is the wellbeing plateau — the one nobody costs at all. Years that are fine, never bad enough to force a change, accumulate into a long stretch of fine. You acclimate. The plateau stops registering as a plateau because it's just the altitude you live at now. None of these arrives as a shock. They arrive as a drift, and a drift is the hardest kind of cost to see, because on any given day there's nothing to see.

The baseline has odds, like everything else

Here's the move. The branch where you stay is not exempt from arithmetic. It has a probability-weighted distribution of outcomes — a spread of where you might land and how likely each landing is — exactly like the branch where you leave. There's a version where staying compounds beautifully: you deepen, you get senior, the field rewards loyalty. There's a version where it leaks. Both are on the branch, each with a weight, and the expected value of staying is just those outcomes summed by their odds.

Once you say it that way, the asymmetry in how we treat the two choices looks absurd. We demand that the bold move justify itself — what are the odds it works, what's the downside, what do I lose if it fails — and we wave the safe move through without an interview. But the safe move is a bet with a distribution, and it can absolutely be the right bet. Staying is often the highest-EV branch on the tree. The point is not that you should leave. The point is that you can't know whether you should until you've priced both branches the same way, and most people only ever price one.

Why we get this wrong every time

This isn't a personal failing; it's wiring. Two well-documented quirks conspire to make the baseline look cheaper than it is.

The first is status-quo bias: across experiments and real decisions — health plans, retirement allocations — people stick with the default far more than their actual preferences justify, simply because it is the default (Samuelson & Zeckhauser, 1988). The current state gets a discount it didn't earn. The second is loss aversion: a loss looms larger than an equivalent gain, so we weight the visible, concrete downside of moving far more heavily than the invisible, diffuse downside of staying (Tversky & Kahneman, 1991). The leak on the baseline branch is a loss too — it's just not shaped like one we know how to fear.

Put those together and you get a mind that systematically overprices the bold branch and underprices the safe one. The safe choice isn't actually safer. It just hides its risk better, and our wiring rewards exactly that kind of hiding.

Make "safe" earn the label

There's only one cure, and it's not "be braver." Bravery is just buying the bold branch at an inflated price — the same mistake, mirror-image. The cure is to put the baseline on the same axes as everything else: the same time horizon, the same outcome spread, the same honest accounting of where it leads and how likely each ending is.

Do that and one of two things happens. Either staying comes out ahead on its own merits — in which case you've earned a calm you couldn't have had while it was unexamined — or it doesn't, and you've found a leak in time to patch it. Both are wins. The only losing move is the one most of us make by default: leaving the baseline unpriced, calling it safe because we never looked, and betting the whole decade on it blind.

The safe choice can be the right one. It just has to earn the label.

Journal of Risk and Uncertainty · Samuelson & Zeckhauser (1988)Status Quo Bias in Decision Making — the foundational study on why defaults winQuarterly Journal of Economics · Tversky & Kahneman (1991)Loss Aversion in Riskless Choice: A Reference-Dependent Model